Designers are often among the first built environment sectors to feel the impact of a recession. With economic forecasts getting gloomier by the week, practice leaders are buckling up for a rough ride, writes Tom Lowe

“The only time I’ve chaired one of our operations meetings and there have been no leads coming through at all was during Liz Truss and Kwasi Kwarteng’s government,” says Ben Derbyshire, chair of housing architect HTA Design. “The uncertainty that those two managed to instantaneously create was remarkable”.

Derbyshire’s practice is far from alone in having been temporarily scorched by the economic firestorm which Truss and Kwarteng accidentally whipped up during their brief time in Number 10. It has, all told, been a rough few months for architects.

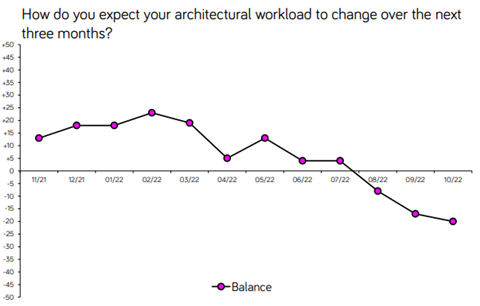

RIBA’s Future Trends survey covering September, the month of the infamous mini-Budget, showed expectations of near-term workloads slump to the lowest level since the first covid lockdown, and nearly to levels not seen since the 2009 financial crisis.

Confidence fell again in October, with nearly 90% of practices expecting workloads to either stay level or slump further. All four sectors covered in the survey, private housing, public sector, commercial and community, continued to slide, while the outlook in London continued to darken. The capital, the architectural sector’s largest market, has now cemented its status as the country’s most pessimistic region.

Derbyshire says the number of enquiries being received at HTA has stabilised following Rishi Sunak and Jeremy Hunt’s efforts to calm the markets. The practice now has a reasonable pipeline that will see them through the next few months barring another disaster such as an escalation of the Ukraine war, he says.

But the mini-Budget fiasco is likely to just be the explosive opening salvo of a longer downturn that will put the entire built environment sector under sustained pressure. The OECD said last month the UK would contract more than any other nation in the G7 next year. The Office for Budget Responsibility has predicted the UK economy will shrink by 1.4% in 2023, with growth of just 1.3% in 2024.

The wider economy did grow by 0.5% in October compared to the previous month, but this has been interpreted as a rebound after output was hit by the extra bank holiday in September for the funeral of Queen Elizabeth. Hunt warned the situation will get worse before it gets better, having said in last month’s Autumn Statement that the country was already in recession.

The Construction Products Association has sharply revised down its forecast for construction output next year from a decline of 0.4% to 3.9%, with private housing activity now expected to plummet by 9%. The latest S&P Global/CIPS UK Construction PMI report has found market confidence among construction buyers was at its lowest since May 2020, at the start of the covid pandemic.

None of this is good news for architects, who are often among the first to feel the impact of trouble in the built environment sector. So how are practices planning for what could be a prolonged period of dwindling work opportunities?

The answer many are giving is diversification. The increasing scarcity of work in London is prompting practices to look further afield into regions with comparatively higher growth, like Manchester and Bristol. Remote working is also making it easier to access global markets, with clients more open to working with practices who operate in different countries than they were before the pandemic. Others are looking for different types of work, such as speculative feasibility studies for developers which want to ensure they have a pipeline ready to go when the market improves and it is safe to build again.

Weston Williamson & Partners has been putting down roots in new markets to ensure a broader base, according to chief operating officer Geoff Bee. “It’s concerning, but we’ve been diversifying across the country looking at different regions, and Scotland and Wales, and also across the globe so we believe we’re relatively well positioned,” he says. “There’s a whole series of wider opportunities across different regions which is where we’re focusing, not only the big projects but on the smaller projects where local growth can occur”.

BE1 Architects is another practice which is focusing more attention on areas outside the capital. Director Ivan Soldo says the practice, which has 11 staff, is refusing to allow its confidence to be kicked by the economic forecasts.

“If anything we’re investing…the next couple of years might be slightly more difficult so why not outweigh that with extra investment now, so we’re looking potentially at the North West of England to expand and tackle that area where we’re a little bit less represented,” he says. “If we slow down to 80% turnover over the coming 12 months, at least there’s another stream of work coming potentially from regions where we have seen opportunities.”

The practice is also looking at increasing its involvement in projects at earlier RIBA stages. Soldo expects work for executive architects, those working during the construction stage of projects, to be harder to find as builders get cold feet on schemes. He says some developers which in the past might have given a confident outlook are making more enquiries about feasibility studies on sites.

“The strategy when you see construction prices going up and mortgages being a bit heavier to procure, housebuilders rethink,” he says. “So they say ‘why don’t we expand our portfolio so when things get better for the buyers then we can be a bit more aggressive on building houses, so let’s expand our stock of land, we can always sell or build on it later’”.

Anecdotally, there have been reports of increasing numbers of developers pulling out of projects. “It’s definitely something we’re hearing,” says RIBA head of economic research and analysis Adrian Malleson. “Clients are backing out of projects when the costs have become clearer, because the costs have accelerated so much during the design stages.” One housing practice, who wanted to remain off the record, said the experience had taught them to focus on projects “that we think are more propitious and that seems to have served us well.”

But there are potential growth sectors which Malleson says practices could pay more attention to. Private healthcare is expected to expand, as people with money look for alternatives to the long waiting lists currently blighting the NHS. Another is education, spurred by increasing numbers of non-EU students, and student accommodation, of which there is a chronic shortage in some key cities.

One silver lining on the recent Future Trends surveys is a sturdy outlook for staffing levels. Practices are keen to retain their staff, despite an expected reduction in workloads. Malleson believes this is partly down to Brexit, which has tightened the jobs market due to stricter immigration rules and a general sense among overseas workers that the UK is not as welcoming as it once was.

“What that’s brought to bear is that it’s been quite difficult for large and medium practices to recruit and retain talent,” he says. “What I think they’re trying to do is to retain the staff they have so they see it’s worth investing longer term in staff maintenance, so they’re ready for the uptick rather than laying off and being disadvantaged in the longer term.”

> Also read: If we are heading into a downturn, it’s not yet impacting the jobs market

For Soldo, retaining staff is about reassuring clients. “My thinking has always been that it is better to stay the course with the current numbers or potentially expand rather than shrink down.

“If you project confidence, if you’re aggressive with business development, you continue delivering satisfactory, excellent design, you will keep your clients….Call us a bit naive but that’s how we are approaching it as of now.”

Neither are there plans to cut numbers at HTA. “We haven’t laid off staff and we’re not talking about laying off staff either,” says Derbyshire. More than 90% of practices expect to employ more staff or increase their headcount over the next three months, according to the latest RIBA report. This is more pronounced with larger practices, those with at least 11 staff.

But how long will this last if the economic situation continues to worsen? “I think in the broader economic context those medium and larger size practices still face quite significant challenges,” Malleson admits.

“To put it pretty crudely you’ve got a lot of money being sucked out of the economy on one side by monetary policy with an increase in interest rates, and fiscal policy, so that’s going to have a direct effect on longer term capital expenditure, because while project cost inflation is starting to settle down a little bit, interest rates have added a new degree of cost to longer term projects.”

It is not clear yet how deep or long the recession will be. Inflation is expected to peak at 11.1% in the last quarter of this year before coming down in the spring, according to the CBI, although we have heard that before. The relaxation of China’s zero covid policy after recent protests in the country could help ease supply chain issues, which might see prices starting to settle. Whatever lies ahead, Malleson says he trusts in the ability of architects to be “resilient and to adapt and to look for new markets and to create innovative solutions to economic and spatial problems”.

And he says there is one market where architects are needed more than ever: addressing climate change. “Beyond this one or two year slump, the need for architectural work in addressing the climate emergency is not going to go away”.

2 Readers' comments