Future Trends survey finds growing confidence gap, with larger firms increasingly optimistic about workload and staffing growth

A contraction in domestic-housing design work is casting a pall over smaller architecture practices, underpinning a worsening outlook for staffing levels and work pipelines across the whole sector, according to RIBA’s latest survey of industry sentiment.

The institute’s crunch of Future Trends responses from some 122 practices across the nation found the sector as a whole more downbeat about future workloads and staffing levels last month than was the case July.

However, RIBA said responses showed a widening “optimism gap” between larger practices and their smaller counterparts, who traditionally undertake a greater proportion of housing work. It said smaller firms were “markedly less hopeful” about future work pipelines.

The Future Trends Workload Index found 18% of practices expect workloads to increase over the coming three months, 29% expect them to decrease, and 53% expect them to stay the same. The overall index score was -11, a slight decrease on July.

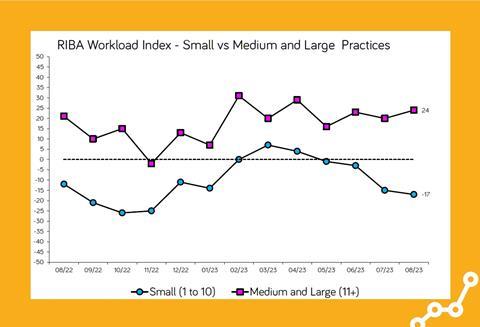

Filtered by business size, optimism among practices with 10 or fewer staff dropped to -17 on the index, in contrast with increasing positivity about future workloads among practices with 11 or more staff. The combined Workload Index score for medium- and large-sized practices was +24, a four-point increase on July’s figure.

Expectations on headcount worsened slightly from July, with 13% of practices expecting to employ fewer permanent staff over the next three months, 12% expecting to employ more, and 75% expecting no change. Filtered by business size, small practices expect staffing to decline while medium- and large-sized companies are expecting an increase.

RIBA head of economic research and analysis Adrian Malleson said the survey’s findings reflected the “downbeat context” of the UK construction sector, with rising interest rates making project financing more expensive and harder to obtain.

“The housing sector is the worst hit, with confidence in the sector at its lowest since the pandemic, affecting smaller practices the most. Larger practices, typically with a more diverse portfolio and less reliant on housing, are consistently more optimistic,” he said.

“This month’s feedback from practices underscores the tightening market, particularly in domestic housing. Practices report significantly fewer new enquiries for residential projects, and existing projects being put on hold, as obtaining financing becomes more challenging for existing and potential clients.”

Malleson added that architects were also reporting planning-system delays still impeding project progress and ongoing difficulties in recruiting and retaining high-skilled staff.

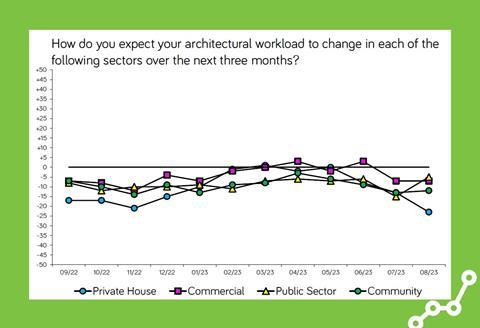

While all four of RIBA’s monitored work sectors have a negative outlook for future work, housing was the only one that worsened from July, dropping 10 points on the Workload Index to -23. Expectations of work in the public sector and community sector improved in August to -5 and -12 respectively. Workload expectations in the commercial sector remained unchanged at -7.

Except for the South of England, the regional picture of sentiment on future workload deteriorated further from July to August, and no region had a positive outlook. Nevertheless, Wales and the West and the South of England both anticipated growing staff levels over the coming three months.

Downloads

RIBA Future Trends Report Aug 2023pdf

PDF, Size 0.11 mb

1 Readers' comment