Joey Gardiner studies the numbers and asks how much damage has already been done to UK construction – and, talk of truces and ceasefires not withstanding – how bad things could still get?

Yesterday’s UK construction purchasing managers’ index data was stark evidence – if it were needed – of the impact the Iran war is already having on the UK economy. It recorded output declining, with the index at its lowest since the pre-Budget downturn last November – a whisker away from being the lowest since the covid crisis.

The cause? Emptying order books amid sharply rising construction prices linked to the increasing cost of oil, according to S&P Global, which runs the index. Tim Moore, economics director at S&P Global Market Intelligence, said: “Aside from the post-pandemic surge in input prices from early-2021 to mid-2022, the latest rise in purchasing costs was the steepest in three decades of data collection.”

Last week, the price of oil hit $126 per barrel, its highest since the early days of the Ukraine war. While it has since come down amid current talk of an imminent deal, previous hopes of ending the war have proved illusory. The potential global impacts of oil priced at that level are enormous, ranging from food supply to, of course, the economy.

Nobel Prize-winning economist Paul Krugman said recently that “a full-on global recession is more likely than not” if the Strait remained closed for another three months. He is not alone: A report by Oxford Economics, modelling a “prolonged war” scenario, said this would cause oil prices to hit nearly $200 per barrel, “tip[ping] the world into outright contraction”.

The impacts are already being felt in the UK development and construction sector. A slew of trading updates from housebuilders in recent weeks has flagged increasing build costs coming down the line, and the first signs of nervousness from buyers, with Taylor Wimpey reporting a 1% price drop. Crest Nicholson has already been so badly hit by the stalling land market that it is in discussions with its lenders to relax its loan covenants.

Building now understands that some in the listed housebuilding sector are modelling worst-case scenarios of potential build cost rises next year of up to 25%. The question, then, on everyone’s lips, is how damaging is the current situation? And, further, how bad might it be if it continues?

Demand is holding – for now

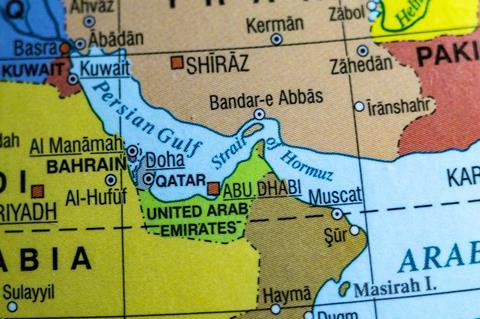

The most obvious answers to those questions, are of course that it will depend on how long the conflict goes on, how long the Strait of Hormuz remains closed, whether it stays open if and when it reopens and how long it then takes to return the volume of oil and other goods transported to their previous levels. All of which is, of course, not in the hands of the UK construction sector.

What can be estimated, however, is what the impact has already been – and what other effects are effectively “in the post” from the conflict so far. Analysts say the closure of the Strait of Hormuz and the rise in oil prices is twofold.

Firstly, it chokes off demand through higher borrowing costs, damage to economic growth and by reducing consumer and business confidence. Secondly, it hits the supply side by increasing build costs, mostly with higher materials prices.

So far, in the housing market at least, demand has held relatively steady. This is despite the fact that average mortgage rates have risen by just shy of 1% since the outbreak of the war on 28 February.

A couple of weeks ago, Barratt, the UK’s largest housebuilder, reported a “resilient” market, with sales rates in 2026 ahead of the same quarter last year. Persimmon last week told a similar story. Even Taylor Wimpey, which reported a 1% price drop in the latest quarter, described demand as “steady”.

Will steady demand continue?

“Sales have remained more resilient than we expected,” one listed builder insider says. “We’re kind of waiting for the cliff edge to come.

“We’ve seen a decline in website traffic and people visiting sites, but the conversion rates are good from those we get.”

The problem is, there is little confidence that this situation will last.

Emily Williams, director in the residential research team at agent Savills, says many of those in the market in the past two months will have been people who agreed a mortgage in principle prior to the conflict starting – and so will have had an extra incentive to complete their purchase at the pre-war rate prior to that offer expiring.

“That effect will wind down in the next month or so,” she adds. “A significant drop in activity is a risk.”

Alastair Stewart, construction analyst at Progressive Equity Research, agrees. “For the first few weeks, trading has all been fine,” he says. “But war’s not a good look and over time these mortgage offers will expire.”

The most recent builder to update, MJ Gleeson, may be a straw in the wind on this: it said last Friday that it had recently seen “some softening” in both footfall and reservations. In addition, the demand picture is varied across the country, with Scotland and the north and midlands seen as performing most strongly. Conversely, both Taylor Wimpey’s and Crest Nicholson’s updates mentioned market weakness in the south of England, with Crest reining in sales expectations for the year.

Scotland and the north is good at the moment. The further south you go, it gets worse, and London is just a basket case

Housing industry insider

A separate housebuilding industry insider said: “Scotland and the north is good at the moment. The further south you go, it gets worse, and London is just a basket case.”

Hence, despite ongoing sales, housebuilders including Barratt, Taylor Wimpey and Persimmon have all said that they are reining in their land buying activity, with the London-focused Berkeley halting completely. It said fears that the war would halt the housing market recovery had “now become a reality”.

Rising materials costs

The more immediate concern for most is on the supply side, with build costs already starting to rise, according to the updates from Taylor Wimpey, Crest, Persimmon and Barratt Redrow. These have flagged an additional 2% to 2.5% extra on build inflation this year, pretty much doubling what was previously expected. Charlie Campbell, equity research MD at investment bank Stifel, says this uptick is consistent with the cost of materials increasing by a fifth.

A blog by Noble Francis, economics director at the Construction Products Association, says the price impact on oil-based based products – such as plastic piping and insulation – has been immediate, while the impact on energy-intensive products takes longer to flow through, given that energy contracts may not immediately reflect higher prices. Energy-intensive products include concrete, bricks and steel. He says he expects 14% to 16% materials price inflation, assuming oil prices stay above $100 a barrel for four months in total.

There is already direct evidence from builders’ merchants that prices are going up. Price notifications sent out by trade suppliers Primaflow F&P, James Burrell Builders Merchants, and BSS Industrial, for example, all show rises across a wide range of products flagged for last month, this month, June and July.

These include brands such as Kingspan and Polypipe, with rises cited of anything between 1% and 20%. In addition, the James Burrell list shows some products are applying a further “temporary surcharge” to pay for transport costs during the “ongoing conflict in the Middle East”.

Cement is an energy-intensive industry, so the war is already impacting the cost of production

Martin Casey, Mineral Products Association

Martin Casey, senior director for cement and lime at the Mineral Products Association, says the government should be assisting the sector by keeping energy costs down, otherwise prices will rise. “Cement is an energy-intensive industry, so the war is already impacting the cost of production,” he says.

Likewise, Jonathan Clemens, chief executive of the British Constructional Steelwork Association, says steel prices are “highly sensitive” to energy costs, with the risk that “panic buying” creates short term shortages.

“If energy prices remain elevated, the impact will inevitably work its way to project costs,” he says. “At this time our members have seen increases of 12% to 15%, directly attributable to the impact on energy prices and the panic buying the fears of shortages and further increases has caused.”

How the war is affecting construction contracts

People tendering and negotiating construction contracts are responding in a variety of ways to the oil price spike, according to commentators. The pressure and volatility on materials prices means that some clients and suppliers have been reluctant to sign deals until the war is resolved, says Simon Rawlinson, head of strategic insight at consultant Arcadis, thereby delaying projects. “People are circling round a bit, hoping the situation resolves itself,” he says.

In addition, the use of contracts with “price adjustment mechanisms” is increasingly common, says Rawlinson, allowing the risk of the fluctuating price of materials to be shared between client and supplier. However, he says that the opposite approach – of suppliers taking risk but putting in “silly figures” to cover that – is also prevalent. “That’s probably the least helpful way to go about it,” he says.

Clients have a responsibility not to slough off risk on suppliers. Paul Beeston, partner at consultant RLB says: “The trend has already been for more collaboration and risk-sharing. Contractors are taking a more diligent approach to risk management given what we’ve seen around insolvencies.

“Clients are having to come to the table with collaboration.”

Iain Parker, director at T&T Alinea, says the industry needs “fair and equitable sharing of risk” during the crisis, “because without this projects and programmes could slow down to a point where nobody wins.”

The impact on overall build prices

Of course, materials do not make up all of the cost of a project. For residential work, housebuilders use a 50-50 rule of thumb that materials and labour costs should be pretty equal. And, given the current relatively weak construction market, there is little sense that labour costs are about to rise.

In fact, the weakness of the construction market – S&P’s UK Construction PMI has been registering falling output for 15 months now – means that the extent to which materials price rises will be passed on by trade contractors anxious to win work is unclear.

I’m certainly aware of contractors that are standing behind prices they put in prior to the outbreak of the war. Securing workload is really important at the moment

Simon Rawlinson, Arcadis

Simon Rawlinson, head of strategic research at consultant Arcadis, says: “I’m certainly aware of contractors that are standing behind prices they put in prior to the outbreak of the war. Securing workload is really important at the moment.”

While the immediate parallel to now is the energy crisis prompted by the outbreak of the Ukraine war in 2022, after which materials prices spiked by 25%, the state of the economy means many expect the inflationary impact to be less – so long as the war is brief. Paul Beeston, partner at consultant RLB, says: “You’ve got an interesting dynamic because construction pipelines are not as full as they were. Keeping order books full is in suppliers’ minds, and this means there may be some capacity to absorb price rises.”

Keeping order books full is in suppliers’ minds, and this means there may be some capacity to absorb price rises

Paul Beeston, RLB

RLB in March predicted 3.45% tender price inflation for 2026, and Beeston says this will be revised upwards in June, with the caveat that inflation will be two to three percentage points higher in hotter markets like data centres, where order books are still full and buildings require significant complex plant and equipment from overseas.

Arcadis’ Rawlinson, likewise, sees overall build costs for commercial and high-rise residential going up by between 2.5% and 4% this year. This may not sound like a lot, but with viability already challenged, it could still be a serious hit for some schemes.

If the oil price stays high

None of this, however, accounts for what happens if the situation around the Strait of Hormuz remains unresolved for a much longer period. Even the existing situation impacts upon development at a time when projects are already strained by years of rising prices – and what the industry sees as the cost of excessive regulation – with Zoopla last year claiming half of all housing sites were technically unviable.

Trade body the Home Builders Federation (HBF) is about to issue a report claiming that the combined cost of construction inflation and new regulations on the price of a house over the past five years already amounts to £70,000. Neil Jefferson, chief executive of the HBF, says that without action by the government on this, the number of homes being built will fall.

Any additional pressures would almost certainly lead to a further reduction in housing delivery

Neil Jefferson, HBF

“If the conflict continues, there is clear potential for further rises at a time when recent tax changes and policy costs have already limited developers’ capacity to absorb additional pressures,” he says.

“Any additional pressures would almost certainly lead to a further reduction in housing delivery from levels that are already falling well short of what is needed to meet the government’s ambitious targets.”

The Bank of England said last week that, given an extended oil price shock, it would likely have to raise interest rates in order to tackle inflation – further dampening demand. But in such a scenario, how high could build costs go? Building understands that scenario modelling within the listed housebuilding sector of the impact of the war going into next year has suggested a potential 25% increase in build costs.

One insider said: “It would be next year where it’s all hitting. We’re talking beyond material cost increases, to changes putting real pressure on the sector.”

Such an increase would not only challenge the profitability of housebuilders on new-build, but potentially vastly increase the cost of building safety remediation work, and what the government can expect to get from its £10bn Affordable Homes Programme, the insider said.

How the sector could respond

Another housebuilding insider says firms would have no choice but to slash build rates and cut staff in such a scenario. “Housebuilders would just hunker down and conserve cash – stop buying land, stop building, and slow anything that might increase your work in progress (WIP),” the insider says.

Housebuilders would just hunker down and conserve cash – stop buying land, stop building, and slow anything that might increase your work in progress

Housing insider

Neal Hudson, founder of research firm Residential Analysts, says his concern is the housebuilders who cut output in the years following the Truss-Kwarteng mini-Budget, but that protected capacity for the recovery could now give up. “The longer this goes on, we’re getting closer to the threshold of permanent underlying destruction of economic capacity,” he says.

“They will start laying off staff. Many had started to build back, but a lot of plans might be wiped out now.”

The industry insider says: “The pressure on WIP, on headcount and on footprint [offices] must be on those businesses that haven’t been expanding. And it must reduce the number of homes tha will be built.”

It is, of course, desperately bad news for the government’s 1.5 million homes target. “It’s all pointing to a system where delivery falls,” Hudson says.

In the context of these fears surrounding an extended conflict, the sector is redoubling calls for government support in the form of a help to buy-style boost to demand. However, despite press speculation, the HBF said it does not believe the government is currently considering introducing such a measure.

Krugman says his big question is now when Trump will prove “willing to accept reality” and come to a deal with Iran that lasts long into the future on nuclear capability and the Strait of Hormuz. The future of UK construction and development appears dependent on getting an answer to the exact same question.

No comments yet